Making Tax Digital for Income Tax sounds complicated. It isn’t.

You just need to:

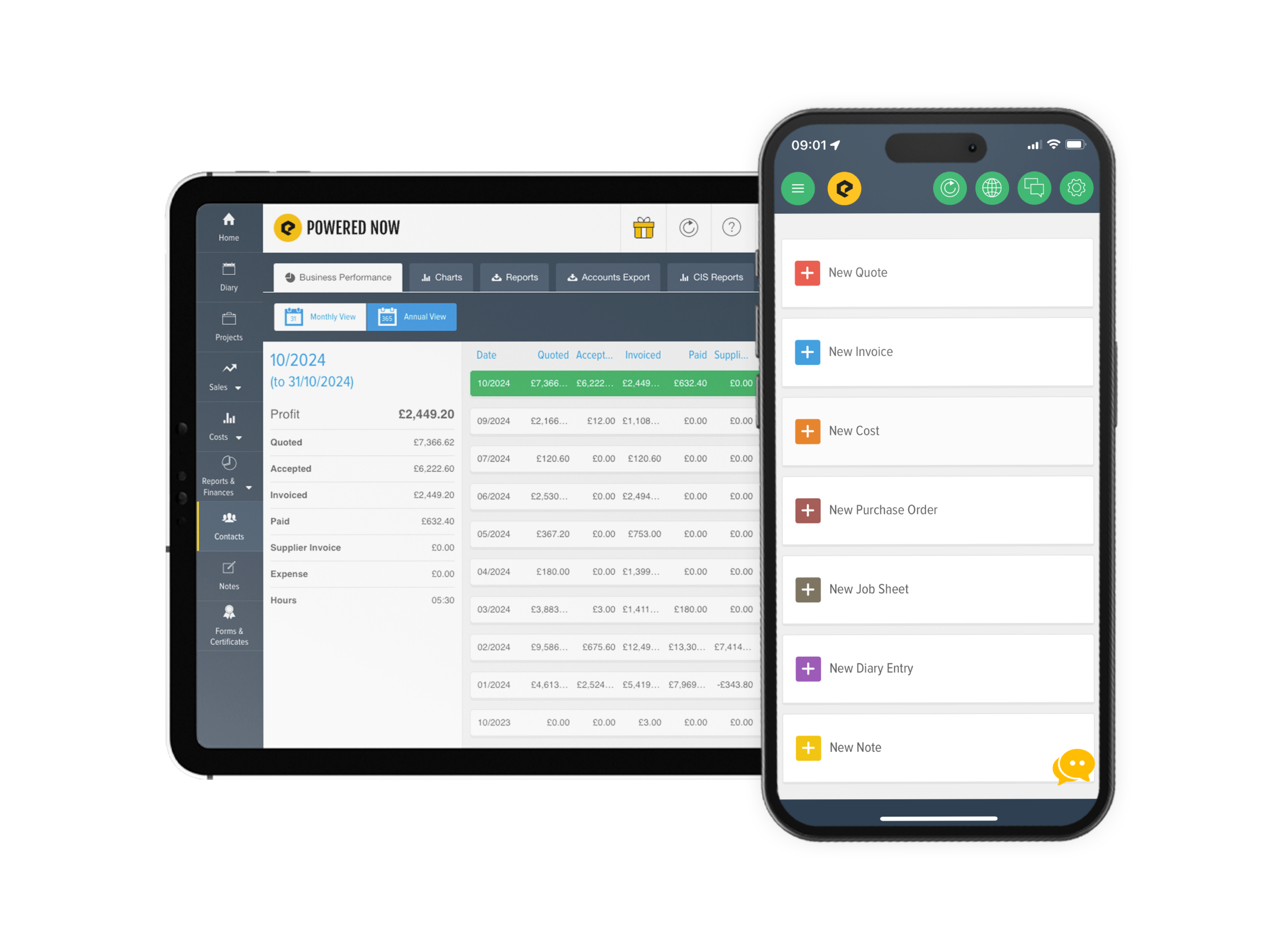

Keep Digital Records of Your Income

Create quotes and invoices as normal in Powered Now. Your income is recorded automatically — no spreadsheets needed.

Record Your Expenses

Log receipts and materials, track fuel and purchases. Everything is stored digitally and organised for you.

Send Updates to HMRC

When it’s time to file, submit directly from the app. Your figures are ready — no last-minute panic.

Then We Do The Rest...

Rated Excellent by UK Tradespeople

How to get started

Tell us a bit about your business and we’ll show you exactly how Powered Now can help you:

Get ready for Making Tax Digital

Save hours every week on admin and paperwork

Get paid faster with professional invoicing

Win more jobs with impressive on-site quoting

What happens next?

Fill in the form to tell us about your business

One of our UK-based team will call you within 24 hours

We’ll give you a personalised demo tailored to your trade

Start your 14-day free trial with full support

Tell us about your business

This helps us understand your needs and tailor our demo to you.

Reviews

Real Stories from Powered Now Customers

Join thousands of happy customers who’ve transformed their trade business

“I run a small electrical business and have been using the app for a while now. Have just upgraded to include certification and other extra features. Really easy to use and saves me lots of time as every thing is in one place.”

Neil Richards

Electrician • Trustpilot

“Powered Now has transformed our business. It has saved us time and money, allowing us to quote, invoice and manage staff from one place. The customer service is excellent with prompt and efficient response from staff.”

Mickey

GroutSolutions • Trustpilot

“I’ve used powers now for quite a few years now and it’s by far the best.

It’s easy to use and easy to navigate and if you do have any questions they are answered straight away

Would have no hesitation in recommending to anyone.”

Marie Barrett

Barrett Heating • Trustpilot

Everything you need to run your trade business

Start your free trial to experience the difference today